.jpg)

Key Takeaways

- Automating claims intake and triage can reduce processing time by up to 50 percent.

- AI-powered fraud detection catches suspicious patterns instantly without delaying legitimate payouts.

- The biggest barrier to claims automation is not AI. It's disconnected systems that can't share data in real time.

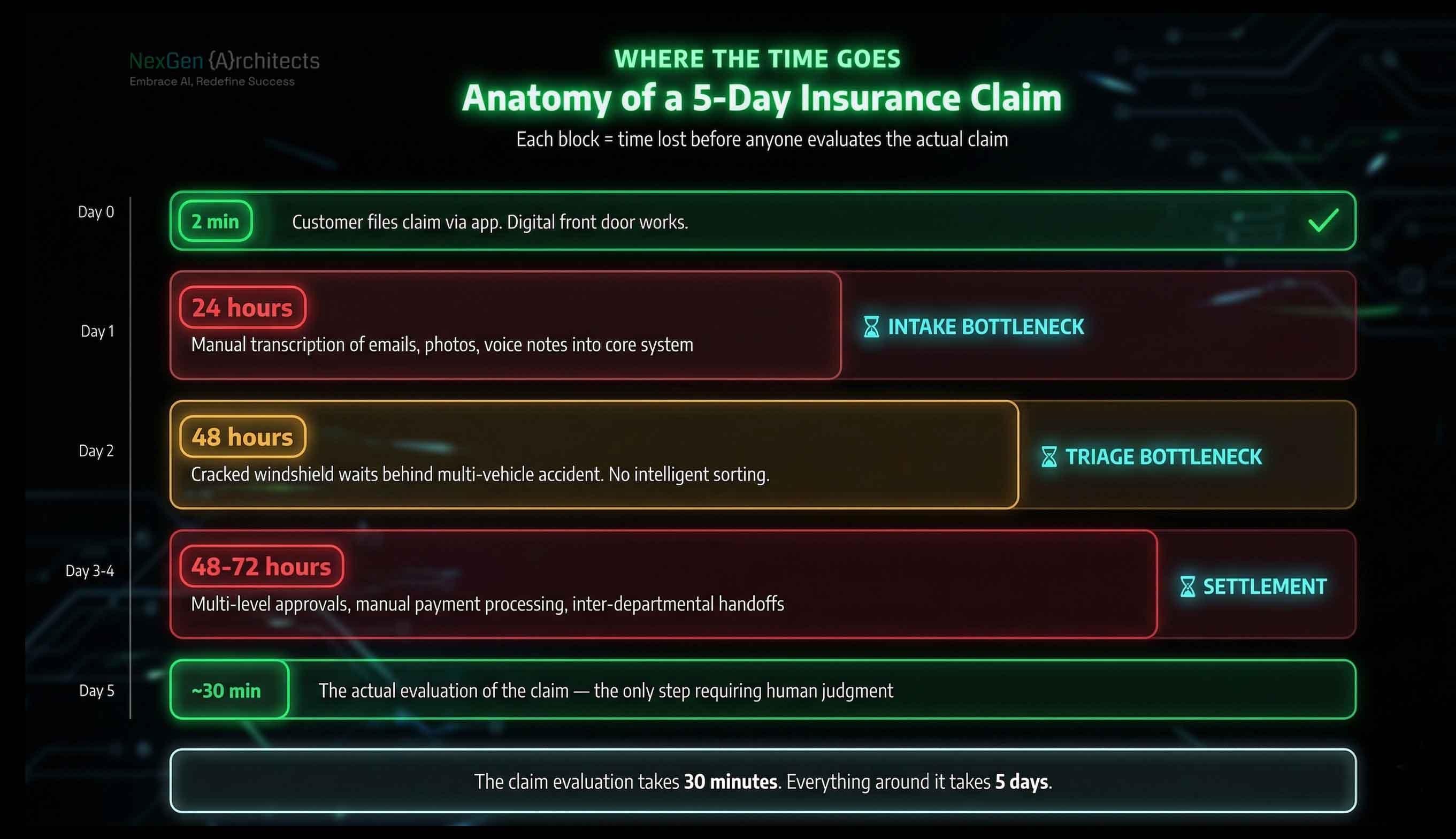

A customer files a claim through a mobile app in two minutes. Then nothing happens for five days. The claim sits in a queue. An adjuster manually pulls up the policy in one system, checks the deductible in another, and cross-references damage photos in a third. By the time someone actually evaluates the claim, the customer has already called twice, posted a complaint online, and started shopping for a new carrier.

This is how most insurance companies still process claims in 2026. The front door is digital. Everything behind it is manual. And the cost shows up everywhere: higher operating expenses, longer claim lifecycles, worse customer satisfaction scores, and lower retention at renewal. According to McKinsey, automation can reduce claims processing time by up to 50 percent. The carriers making that shift are not adding more staff. They are rebuilding how claims move through their systems from the moment they're filed to the moment they're paid.

This blog covers where the bottlenecks actually sit, how AI and automation eliminate them, and what it takes to connect legacy systems so the entire process works as one.

Why Insurance Claims Processing Is Still Slow

Claims stall at three predictable points. First, during intake. A customer submits unstructured information: emails, photos, handwritten descriptions, voice messages. Someone has to manually transcribe all of that into the core system before anything else can happen. That alone can take 24 hours.

Second, during triage. Every claim sits in the same queue regardless of complexity. A cracked windshield waits behind a multi-vehicle commercial accident. Without intelligent sorting, simple claims that could be resolved in minutes sit for days.

Third, during settlement. Multi-level approvals, manual payment processing, and back-and-forth between departments add days to claims that are already verified and ready to pay.

What This Costs Beyond Processing Time

The longer a claim stays open, the more expensive it becomes. Adjusters spend hours compiling data instead of evaluating damage. Error rates increase because of constant context-switching between disconnected screens. And customers who wait too long for a payout leave at renewal. The operational drag of manual claims handling costs carriers millions annually in lost efficiency and lost customers.

How AI Eliminates the Bottlenecks in Claims Processing

AI does not replace the people handling claims. It removes the manual steps that prevent them from doing actual work.

Automated Claims Intake and First Notice of Loss

The first notification is the most critical moment. Modern automation extracts data directly from customer emails, chat messages, or phone calls. The system populates the claim file, verifies the policy, and confirms coverage limits instantly. No manual data entry. No 24-hour lag between the customer reporting an incident and someone opening the file.

The faster that initial data is structured and validated, the faster everything downstream can move.

Intelligent Triage That Separates Simple from Complex

Once the data is captured, AI evaluates the claim against historical patterns. Low-risk, low-dollar claims get routed for fast-track approval automatically. Complex claims involving injuries, disputed liability, or high dollar amounts get assigned immediately to the right person with the right expertise.

This sorting happens in seconds. Routine claims stop clogging the queue. Complex claims get attention faster because the queue isn't backed up with windshield replacements and minor fender benders.

Fraud Detection That Doesn't Slow Down Honest Customers

Fraud costs the insurance industry billions every year. But traditional fraud detection relies on manual audits that delay payouts for everyone, including honest customers.

AI changes this by analyzing patterns across massive datasets in real time. If the same damage photos appear across multiple carriers, or if a claim's details don't match the policyholder's history, the system flags it before anyone even starts processing. Legitimate claims move forward without delay. Suspicious ones get routed to investigation automatically.

The result is faster payouts for real customers and earlier detection for fraudulent ones.

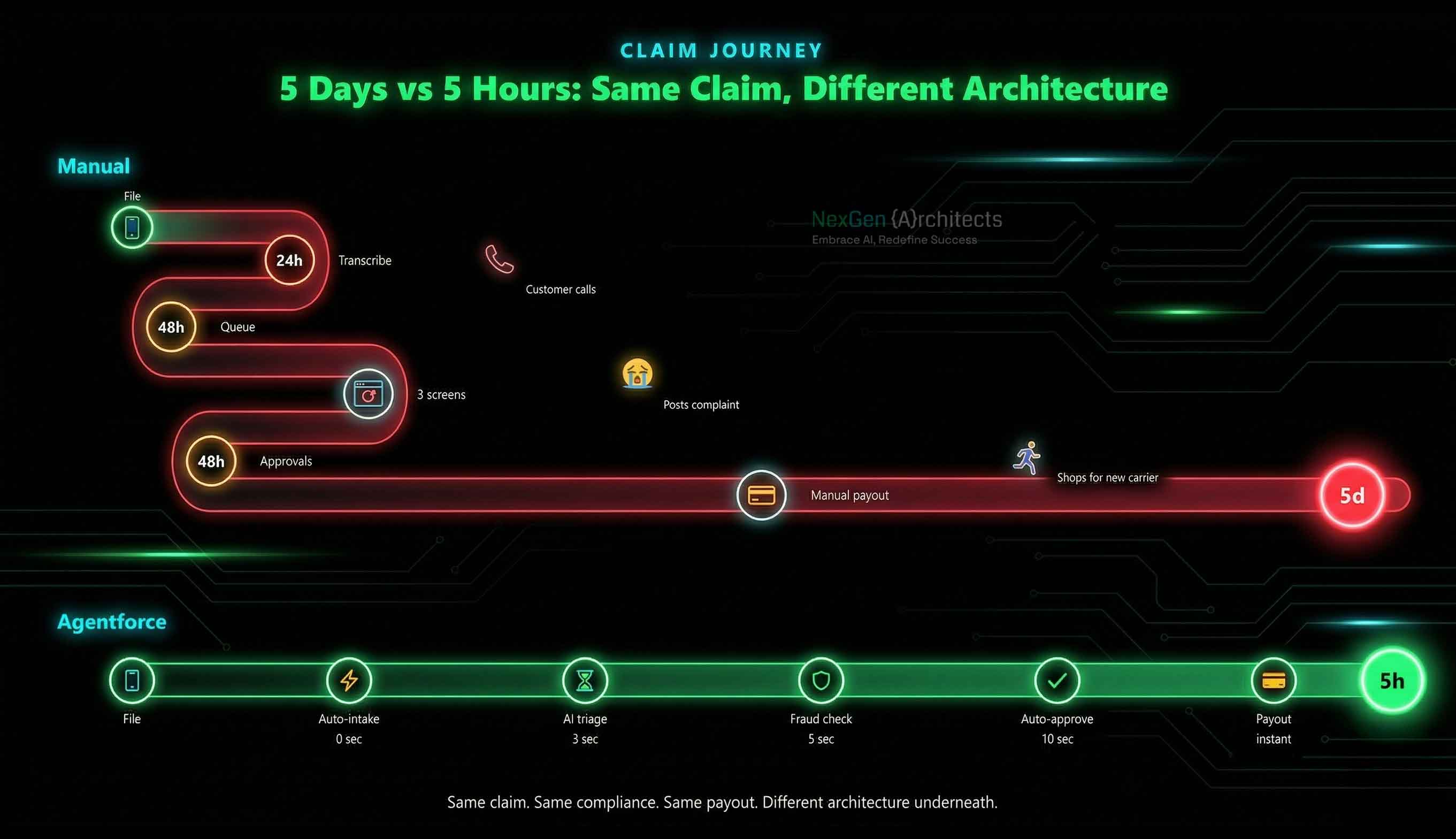

How Agentforce Handles Insurance Claims Autonomously

Agentforce is not a chatbot. Agentforce is an agent that executes workflows. When a policyholder submits a claim for a cracked windshield, the agent verifies coverage, analyses the uploaded photo, calculates the repair estimate, and issues the payment. The entire process completes in minutes without a human touching it.

What Stays Automated and What Gets Escalated

The agent operates within guardrails set by the carrier. If the claim data matches the parameters for auto-approval, Agentforce settles it. If the claim involves bodily injury, unclear liability, or exceeds a dollar threshold, it escalates immediately.

But it doesn't hand over a blank file. Agentforce compiles everything the adjuster needs: a summary of the incident, the specific reasons for escalation, verified policy data, and any flags from the fraud detection layer. The adjuster starts with full context instead of spending two hours assembling it.

This is what changes the economics. The AI handles the volume. The humans handle the judgment calls. Neither one wastes time doing the other's job.

Why Connected Systems Matter More Than AI Tools

The biggest barrier to insurance claims automation is not a lack of AI. It's the inability to connect AI tools to the systems that hold the data. A claim can't be processed automatically if the CRM can't access the policy administration system in real time.

Bridging Legacy Systems Like Guidewire and Duck Creek to Salesforce

Most carriers run core systems like Guidewire or Duck Creek for policy administration while using Salesforce for customer engagement. These systems were never designed to work together. Data lives in silos. Updates in one system don't reflect in the other. Adjusters toggle between three screens to piece together a single claim history.

MuleSoft connects these systems through a governed API layer. When a customer submits a claim through the mobile app, the API pulls the policy data from the backend, feeds it to the AI for evaluation, and pushes the result to the adjuster's dashboard. When a claim status changes in Salesforce, it updates in Guidewire instantly.

This real-time data flow is what makes automation actually work. Without it, AI tools operate on incomplete information and the "automation" just becomes a faster way to get things wrong.

Where to Start with Claims Automation

Trying to automate the entire claims process at once is how transformation projects stall. The carriers getting results are starting narrow and expanding.

Start With the Highest-Volume, Lowest-Complexity Claims

Glass claims, minor property damage, and towing reimbursements. These consume the most adjuster time but require the least judgment. Automate intake and basic triage for these categories first. This proves the approach works, builds internal confidence, and delivers immediate relief to overloaded teams.

Then Expand AI to Assist on Complex Claims

Once routine claims run reliably, use AI to support complex cases. Agentforce compiles case summaries, recommends settlement ranges, and highlights fraud indicators for bodily injury or multi-party liability claims. The AI doesn't make the final call. It prepares everything so the human can make a faster, better-informed decision.

This phased approach is how a mid-sized auto carrier processing 10,000 claims a month cut their average cycle time from five days to five hours for routine claims. The data stopped sitting in queues. The moment a claim was filed, the system either settled it or routed it with full context to the right person.

Conclusion

Claims processing speed is no longer just an operational metric. It directly affects customer retention, operating costs, and competitive position. Customers who get paid in hours stay. Customers who wait a week start looking for alternatives.

The carriers pulling ahead in 2026 are not the ones with the most adjusters. They are the ones that automated the repetitive work, connected their legacy systems, and let their people focus on the claims that actually need human judgment.

The technology to do this exists today. The gap is in the architecture that connects it all together.

Ready to cut your claims processing time from days to hours? Our team builds the integration and AI architecture that makes it happen. Get a free assessment.

Sources:

- McKinsey & Company, Insurance Claims Automation Report 2025

- Salesforce, Agentforce for Insurance Production Metrics 2025-2026

.svg)