Key Takeaways

- The average bank stores customer data across 12 to 15 disconnected systems, making a complete customer view impossible without an integration strategy.

- A unified customer 360 in Salesforce Financial Services Cloud reduces onboarding time, improves retention, and gives relationship managers the context they need before every conversation.

- The banks achieving real customer 360 are the ones that connected their core banking, CRM, and digital channels through a governed integration layer first.

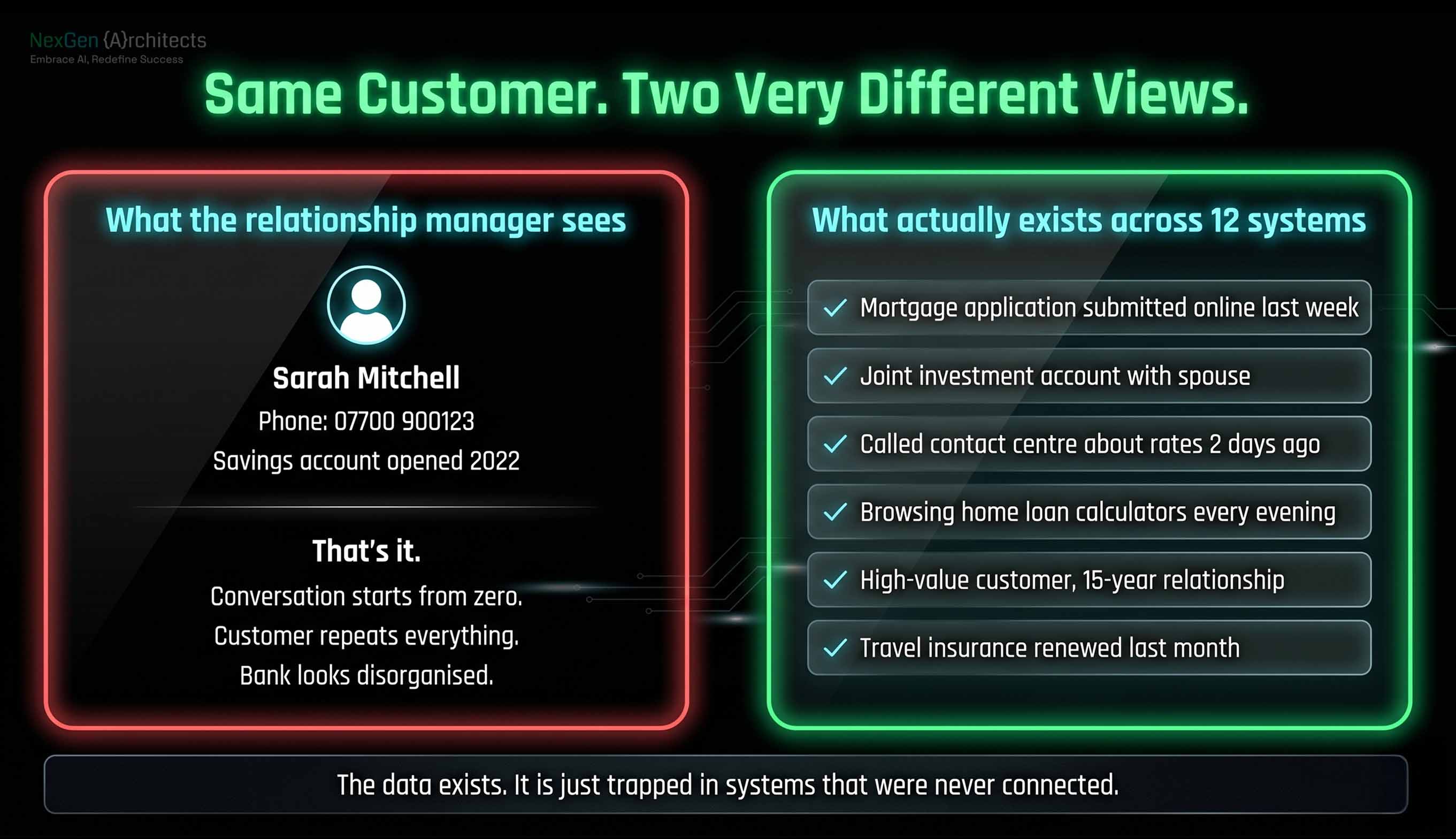

A customer walks into a branch to discuss their mortgage options. The relationship manager opens the CRM. It shows the customer's name, phone number, and a savings account opened three years ago.

What it does not show: the customer already applied for a mortgage online last week. They have a joint investment account with their spouse at the same bank. They called the contact centre two days ago with a question about interest rates. They have been browsing home loan calculators on the bank's website every evening for the past month.

The relationship manager starts the conversation from zero. The customer repeats everything. The bank looks disorganised. The competitor down the road, who unified their customer data last year, already sent the customer a pre-approved offer based on their browsing behaviour and deposit history.

This is what happens when customer data in banking lives in 12 to 15 systems that were never designed to share information.

What Is a 360° Customer View in Banking and Why Does It Matter?

A customer 360 view in banking means every team across the bank sees the same complete profile for every customer: their products, transaction history, service interactions, digital behaviour, risk profile, and relationship context. All in one place. Updated in real time.

Most banks believe they already have this. They have a CRM. They have a core banking system. They have digital analytics. But each one holds a fragment of the customer. The CRM knows the relationship history. The core banking system knows the balances. The digital platform knows the browsing behaviour. The contact centre knows the complaints. Nobody sees the full picture.

According to Salesforce research, financial services organisations that implement a unified customer view see measurable improvements across three areas:

- Retention: Customers who feel understood stay longer. Banks with unified customer profiles identify at-risk customers before they leave, based on behavioural changes that isolated systems would never surface.

- Revenue per relationship: Relationship managers who see the full picture make relevant recommendations instead of generic product pushes. Cross-sell conversion improves because the suggestion is based on actual behaviour.

- Operational efficiency: Service agents resolve queries faster because they see the full context without switching between systems. Onboarding accelerates because identity verification, product history, and compliance checks pull from one source.

Why Most Banks Fail at Building a Unified Customer Profile

The obstacle is rarely strategy. Every bank wants a single customer view. The obstacle is architecture. Customer data is scattered across systems that were built in different decades, by different vendors, using different data models.

Data Lives in Silos That Were Never Designed to Connect

A typical mid-sized bank runs separate systems for core banking, CRM, wealth management, lending, credit cards, digital banking, contact centre, and compliance. Each system stores customer data in its own format, with its own identifiers, and its own update frequency.

The core banking system identifies a customer by account number. The CRM uses a contact ID. The digital platform uses a cookie. The contact centre uses a phone number. The same customer exists as four different records across four systems, and nobody knows they are the same person.

Point-to-Point Integrations Make It Worse

Banks that attempt to solve this with direct connections between systems create a web of dependencies that breaks with every upgrade. Ten systems connected point-to-point means 45 individual connections to maintain. Each one is custom-coded, documented inconsistently, and owned by a different team. Adding a new data source means building connections to every existing system individually.

Batch Syncs Create a Customer View That Is Always Behind

Most banks sync customer data between systems overnight. The CRM shows what the customer did yesterday. The relationship manager prepares for a meeting using data that is 12 to 24 hours old. The customer's most recent interaction, the one that triggered the meeting in the first place, is invisible until tomorrow's sync.

How to Build a Real Customer 360 with Salesforce Financial Services Cloud

The banks that have achieved a working customer 360 followed a consistent architecture: Salesforce Financial Services Cloud as the engagement layer, Data Cloud as the unification layer, and MuleSoft as the integration layer connecting everything underneath.

Step 1: Connect Core Banking Data Through MuleSoft

The foundation is connecting your core banking platform to Salesforce through MuleSoft with real-time, event-driven sync. Account balances, transaction history, product holdings, and risk scores flow into Salesforce the moment they change in the source system. The relationship manager always sees the current state.

MuleSoft abstracts the complexity of the core banking system behind governed APIs. When the core banking platform upgrades, you update the API. Everything downstream continues to work.

Step 2: Unify Identity with Salesforce Data Cloud

Data Cloud resolves the identity problem. It ingests customer data from every connected source and uses matching rules to consolidate duplicate records into a single unified profile. The customer who exists as four separate records across four systems becomes one profile with complete history across every channel.

This identity resolution runs continuously. When a customer updates their email through the mobile app, Data Cloud matches it to their existing profile and updates every connected system.

Step 3: Enrich the Profile with Digital and Behavioural Data

Once the core banking data and CRM data are unified, layer in digital behaviour. Website visits, mobile app interactions, email engagement, and marketing responses all flow into the same profile through Data Cloud. The relationship manager sees that the customer has been researching mortgage rates online before the customer even mentions it.

Step 4: Activate the Profile Across Every Channel

A unified profile that sits in a database and never reaches the people who need it is worthless. The final step is activating the customer 360 across every touchpoint:

- Relationship managers see the full profile, AI-generated next-best-action suggestions, and recent digital behaviour before every client meeting

- Service agents see every product, every open case, and every recent interaction the moment the customer contacts the bank, through any channel

- Marketing teams segment and personalise campaigns based on complete behavioural and financial data instead of partial CRM records

- Agentforce uses the unified profile to handle routine queries, trigger proactive outreach, and escalate complex cases to humans with full context

What Changes When the Full Picture Is Finally Visible

The impact shows up in daily operations, measured in time saved, revenue captured, and customers retained.

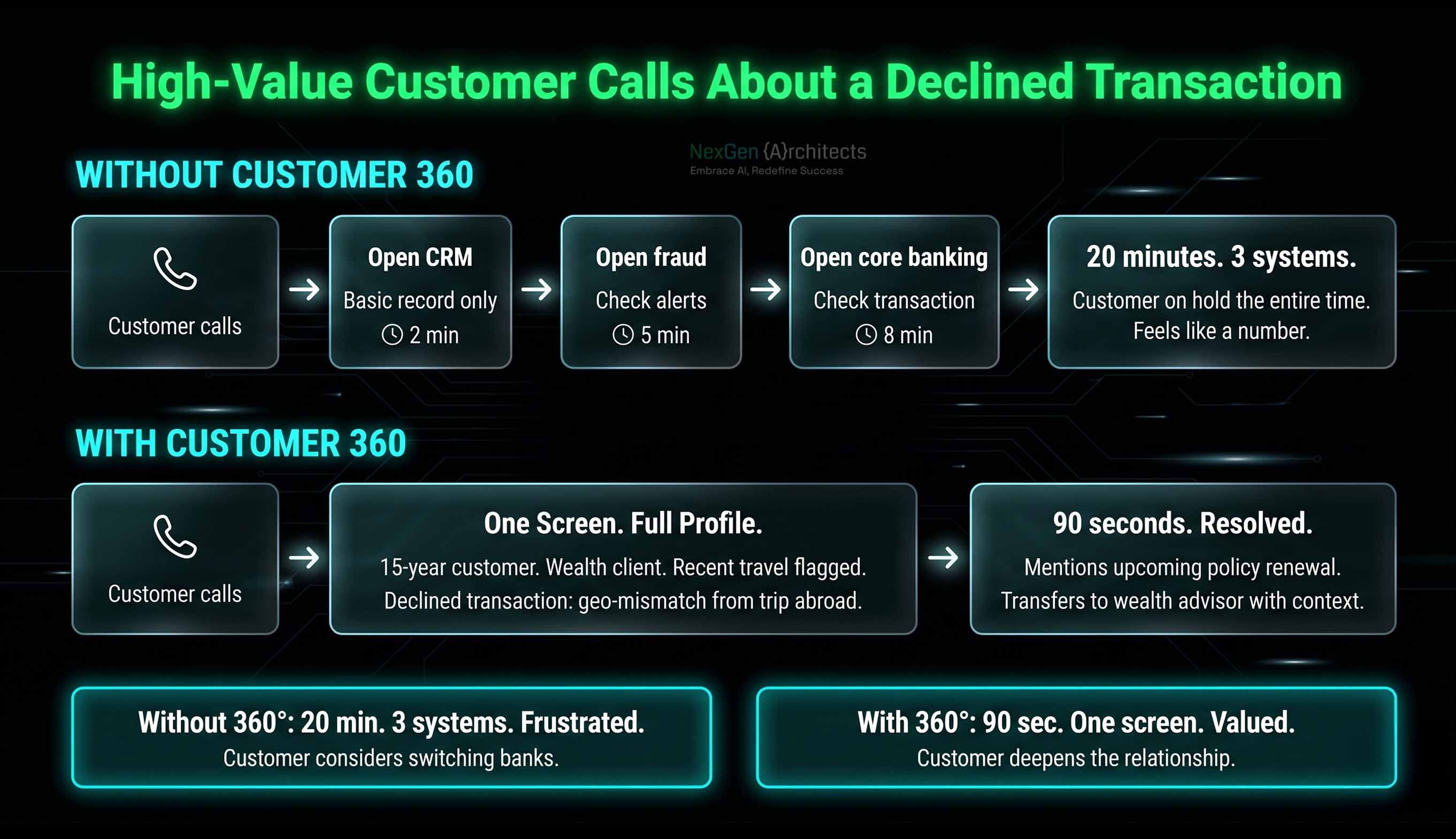

Before the 360° view: A high-value customer calls about a declined transaction. The agent sees the basic account record, puts the customer on hold, opens the fraud system, checks the transaction log in core banking, and calls the customer back 20 minutes later with an answer. The customer is frustrated. They feel like a number.

After the 360° view: The same customer calls. The agent immediately sees their full profile: 15-year relationship, wealth management client, recent international travel flagged in the system, transaction declined due to geo-mismatch. The agent resolves it in 90 seconds, mentions the customer's upcoming policy renewal, and transfers them to their wealth advisor who already has the context. The customer feels valued. They stay.

That is the difference between a database and a relationship.

Conclusion

The banks that built a working customer 360 started with the connection that mattered most: core banking to Salesforce through MuleSoft. They unified identity through Data Cloud. They activated the profile for the teams closest to the customer. Then they expanded.

The ones still planning their "customer 360 strategy" are losing relationships to competitors who already see the full picture.

If your bank is evaluating how to connect core banking, CRM, and digital channels into a unified customer view, connect with us to achieve these exact architectures.

.svg)