No items found.

AI

Jan 30, 2024

Banks spend $72.9M annually on KYC compliance with 90-95% false positive rates. Here's how Agentforce and MuleSoft automate KYC verification and real-time fraud detection

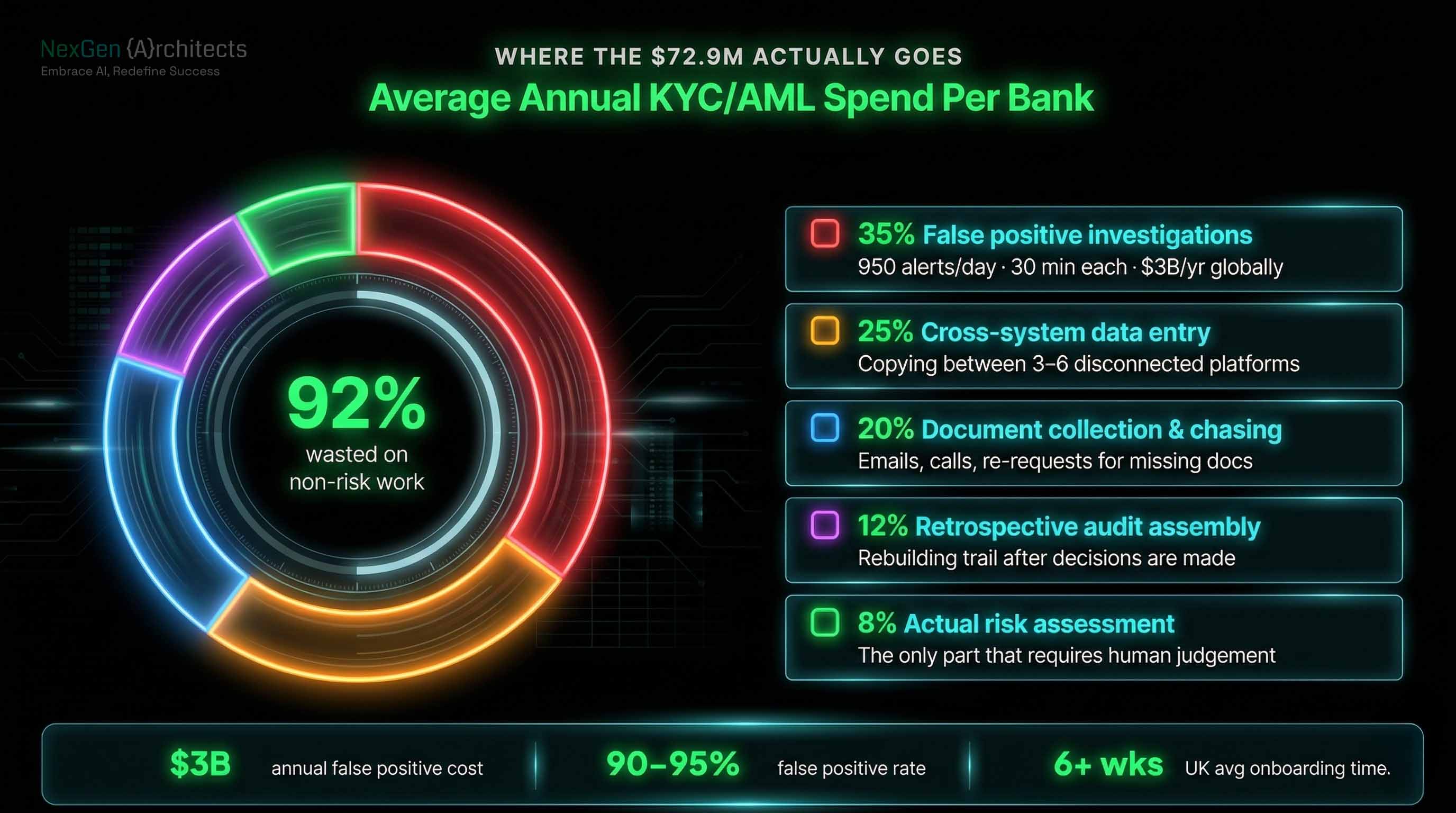

Banks spend an average of $72.9 million per year on KYC and anti-money laundering operations, according to Fenergo's 2025 Financial Crime Industry Trends report. UK institutions spend the most at $78.4 million. And despite that investment, 70% of fraud still occurs after initial KYC checks are completed.

The problem is not a lack of spending. It is a lack of connected systems.

KYC data sits in one platform. Transaction monitoring runs in another. Fraud alerts route through a third. Compliance officers stitch it all together manually, investigating false positives that consume hours and deliver nothing. Global AML alert systems generate false positive rates of 90-95% at large institutions roughly 950 false alerts per day per million transactions processed. Each one takes an average of 30 minutes to investigate.

Agentforce for financial services, launched by Salesforce in 2025, directly addresses this. Autonomous AI agents execute KYC verification, monitor transactions in real time, and flag genuine fraud all connected to core banking systems through MuleSoft integration and grounded in unified customer data from Salesforce Data Cloud.

This article explains how the architecture works, what it replaces, and what banks implementing it are seeing in practice.

KYC is the most time-consuming part of client onboarding in banking. More than half of corporate and institutional banks spend between $1,500 and $3,000 to complete a single client's KYC review, according to Fenergo's survey of 1,000 C-suite executives. One in five spend more than $3,000 per review.

The cost comes from three structural problems that technology investment alone has not solved:

Customer identity documents, credit bureau data, watchlist databases, transaction histories, and risk scores live in separate systems. Compliance analysts manually access each one, copy the results, and assemble a case file. Every handoff introduces delay and error risk.

Most KYC workflows are linear. Document collection must complete before identity verification begins. Verification must complete before risk scoring. Risk scoring must complete before approval. One slow step holds up the entire chain. UK corporate banks report average onboarding times exceeding six weeks.

Transaction monitoring systems flag suspicious activity, but 90-95% of those alerts are false positives at large institutions. Compliance teams investigate each one manually because the systems generating the alerts are not connected to the systems that hold the context needed to dismiss them quickly. The annual cost of false positive investigations alone is estimated at $3 billion globally.

The result: 70% of financial institutions lost clients in the past year due to inefficient onboarding, up from 48% in 2023, with client abandonment rates now averaging around 10%.

Agentforce deploys autonomous AI agents that execute specific compliance tasks independently collecting documents, verifying identities, running watchlist checks, scoring risk, and escalating exceptions without requiring a human to initiate or monitor each step.

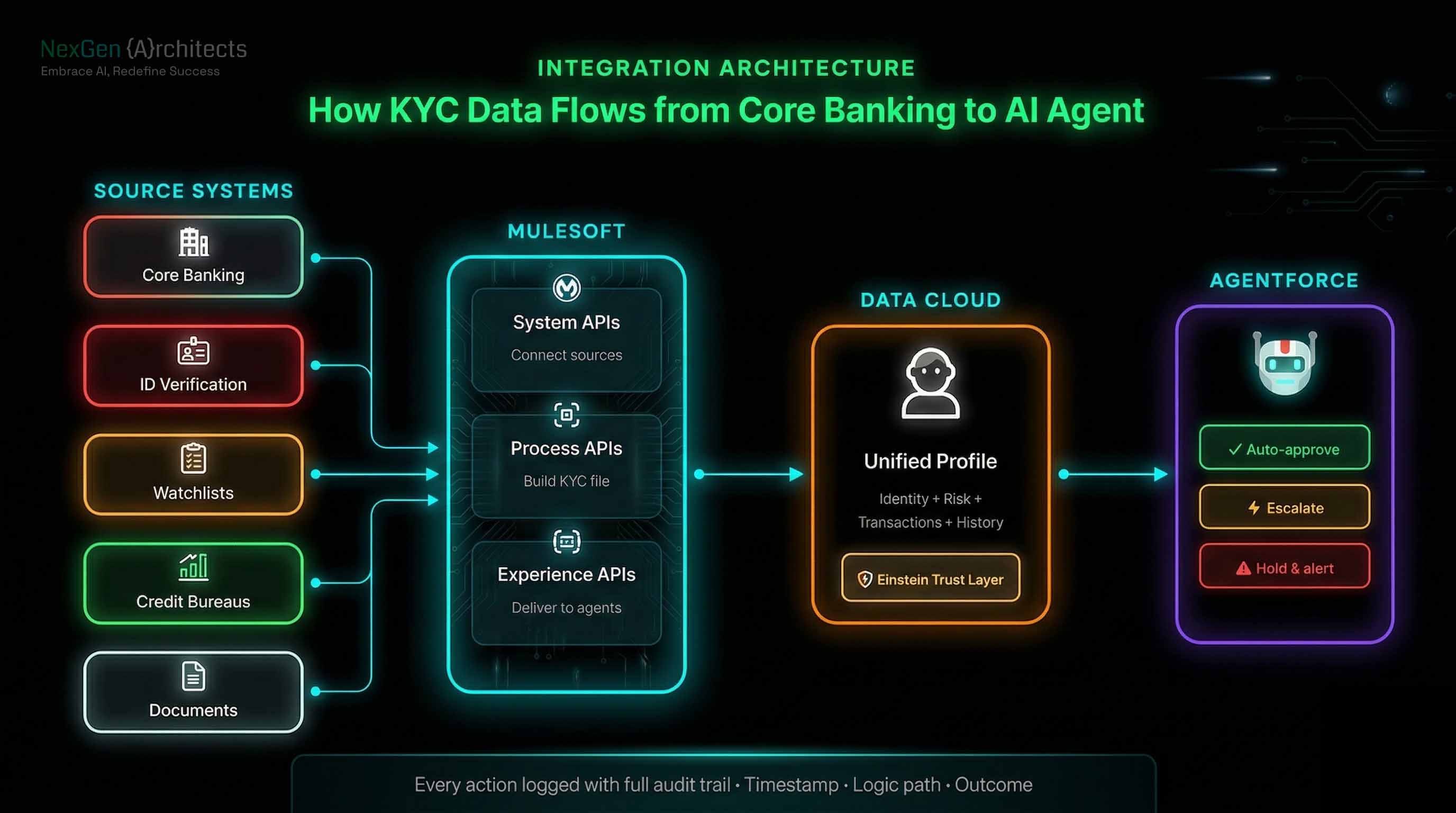

The difference from traditional automation is that Agentforce agents act with context. They are grounded in Salesforce Data Cloud, which unifies customer data from core banking, CRM, document management, and external verification services into a single profile. The agent does not just follow a script. It understands who the customer is, what has already been verified, and what remains outstanding.

Traditional fraud detection systems flag transactions after the fact. An analyst reviews the alert, investigates, and decides whether to act often hours or days later. By then, the money has moved.

Agentforce agents connected to transaction monitoring systems through MuleSoft can act in real time. When an anomaly is detected, the agent cross-references the transaction against the customer's Data Cloud profile — their typical transaction patterns, geographic behaviour, device history, and account activity. If the anomaly is genuine, the agent places an immediate hold, alerts the fraud investigation team, notifies the customer through their preferred channel, and logs every action for the audit trail.

If the transaction matches the customer's established pattern despite triggering a rule, the agent dismisses it automatically and logs the reasoning. This is how Agentforce reduces false positive investigation volume not by lowering detection sensitivity, but by adding contextual intelligence that rule-based systems lack.

Absa Bank, a major African financial institution, has publicly stated that Agentforce resolves customer issues 88% faster while significantly speeding up fraud management through 24/7 agentic support.

Agentforce works on three connected layers working together.

Salesforce Data Cloud ingests and unifies customer data from core banking, CRM, document management, and external sources into a single, real-time customer profile. This profile serves as the grounding context for every agent action. Without it, the agent has no basis for intelligent decision-making.

MuleSoft provides the integration backbone. It connects core banking systems, identity verification providers, watchlist databases, transaction monitoring platforms, and document repositories through API-led connectivity. MuleSoft organises these connections into three reusable layers: System APIs connecting to each source, Process APIs combining data into business capabilities like a complete KYC file, and Experience APIs delivering the right data to Agentforce, compliance dashboards, and customer-facing channels.

Agentforce Studio is where banks define what each agent does. Topics (like "KYC Onboarding" or "Transaction Fraud Review"), actions (verify identity, run watchlist, escalate case), and escalation paths (route high-risk cases to a senior compliance officer via Omni-Channel) are configured in a visual builder. Each action connects to a Salesforce Flow that writes results back to the system of record.

Einstein Trust Layer ensures compliance. All sensitive customer data such as names, dates of birth, account numbers, national identifiers are masked before reaching the AI model. The model generates the response based on masked data. The system unmasks only when delivering actions back to secured internal systems. Every agent action is logged with a complete audit trail: timestamp, prompt, logic path, and outcome.

The KYC software market generated $5.9 billion in 2025 and is projected to reach $43.5 billion by 2034, growing at 24.8% annually. Banks are investing because the results from early automation are measurable:

The banks seeing the fastest ROI from Agentforce follow a consistent pattern: unify customer data first, automate one low-risk workflow, validate, then scale.

Month 1-2: Connect core banking and identity verification systems to Salesforce Data Cloud through MuleSoft. Deploy one agent for low-risk KYC onboarding (standard retail accounts). Monitor performance and audit logs weekly.

Month 3-4: Expand to corporate KYC, periodic reviews, and transaction fraud monitoring. Enable multi-channel customer communication. Connect additional data sources (watchlists, credit bureaus, biometric providers).

Month 5-6: Full automation across onboarding, ongoing monitoring, and fraud detection. Compliance audit-ready at all times. Measure ROI against baseline KYC cost per client and false positive investigation hours.

Banks do not have a KYC technology gap. But they have an integration gap. The data exists. The verification services exist. The compliance rules exist. What is missing is a connected system that allows autonomous agents to access, verify, and act on that data without humans manually stitching it together across disconnected platforms.

Agentforce provides the autonomous capability. The banks that move first on this will not just reduce compliance cost. They will onboard customers faster, detect fraud earlier, and free compliance teams to focus on genuine risk instead of processing paperwork.

Getting the MuleSoft integration layer right, structuring your Salesforce Financial Services Cloud data model correctly, and configuring Data Cloud for real-time customer profiles that is where implementation quality determines whether you see ROI in six months or spend twelve months troubleshooting.

Contact Us if your enterprise is looking for something similar to fix.

.svg)