No items found.

AI

Jan 30, 2024

Loan approvals still take 2–6 weeks while banking customers expect instant service. Here's what's actually causing the delays and how lenders are fixing it.

You can open a bank account in five minutes. Transfer money in seconds. Get a credit score on your phone before breakfast.

But apply for a mortgage or a business loan, and suddenly you're waiting weeks. Phone calls go unanswered. The same documents get uploaded three times to three different places. Nobody seems to know where the application actually is.

The UK processed over £77.6 billion in gross mortgage advances in Q1 2025 alone, a 50.4% increase on the year before, according to the Bank of England. First-time buyer lending hit 31.4%, the highest share since reporting began in 2007. Demand is surging. But the way most lenders process applications hasn't fundamentally changed in over a decade.

This article breaks down what's actually causing delays in loan approvals, where the real bottlenecks are, what it costs lenders in revenue and reputation, and what the fastest-growing firms are doing differently.

The short answer: anywhere from two to six weeks for a straightforward application, according to most UK lenders and the FCA's published guidance. But in practice, that timeline stretches much further for many borrowers.

Several factors influence processing speed:

Self-employed borrowers, non-standard income sources, or properties with unusual characteristics (listed buildings, leasehold complications, new-build snagging) all add time. Lenders need more documentation, more verification, and more manual assessment.

High-street banks with automated decisioning can approve simple applications in under 14 days. Specialist lenders handling complex products second-charge mortgages, bridging finance, commercial loans often take longer because each application requires individual underwriting.

The Bank of England reported 59,999 mortgage approvals in January 2026, down 10% on the previous year. When volumes spike (as they did through most of 2025), processing queues grow. When volumes dip, lenders may reduce staff, creating different bottlenecks.

Incomplete documents, slow responses to queries, and incorrect information all add days or weeks. But this is only part of the story and often the part lenders blame first while ignoring their own operational friction.

The real question isn't whether a specific application is complex. The real question is why even straightforward applications still take weeks in an era when most other financial transactions happen in real time.

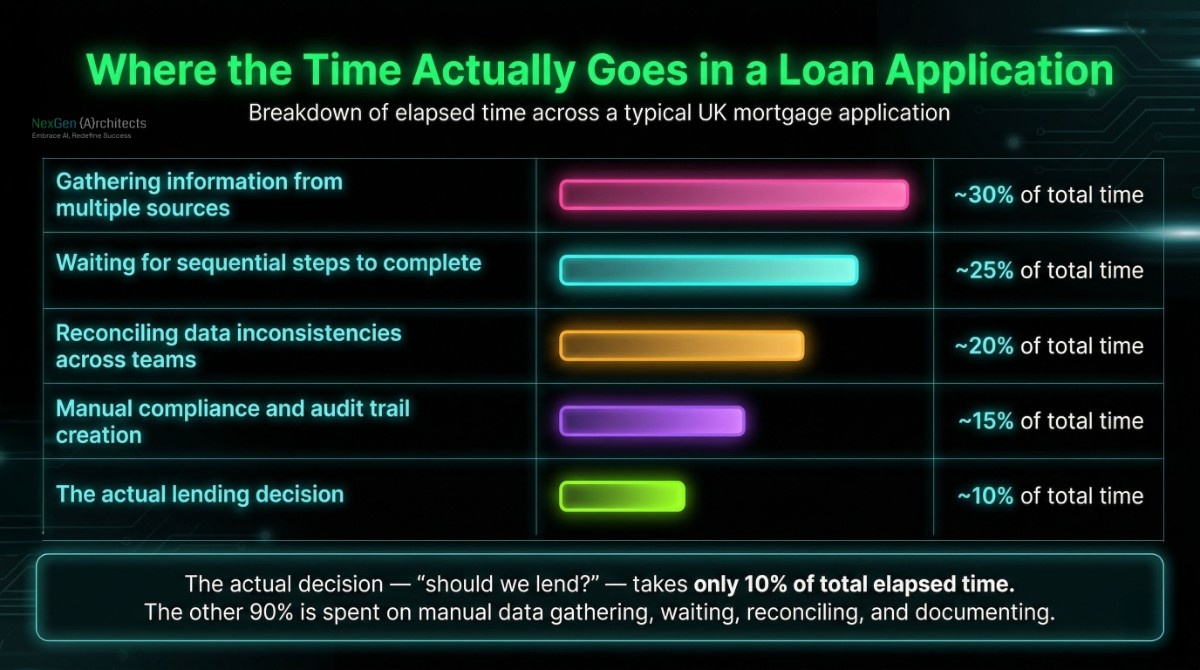

When you map out the full journey of a loan application from initial enquiry to funds being released the actual lending decision ("should we lend to this person?") takes a fraction of the total elapsed time. The rest is consumed by everything around that decision.

Here's where the time actually goes:

A single mortgage application typically requires data from credit reference agencies (Equifax, Experian, TransUnion), property valuation services, employer or accountant references, solicitors, the Land Registry, and the borrower themselves. In many lending firms, staff manually access each of these sources separately, then re-enter the results into their own records. Every handoff introduces delay. Every manual entry introduces error risk.

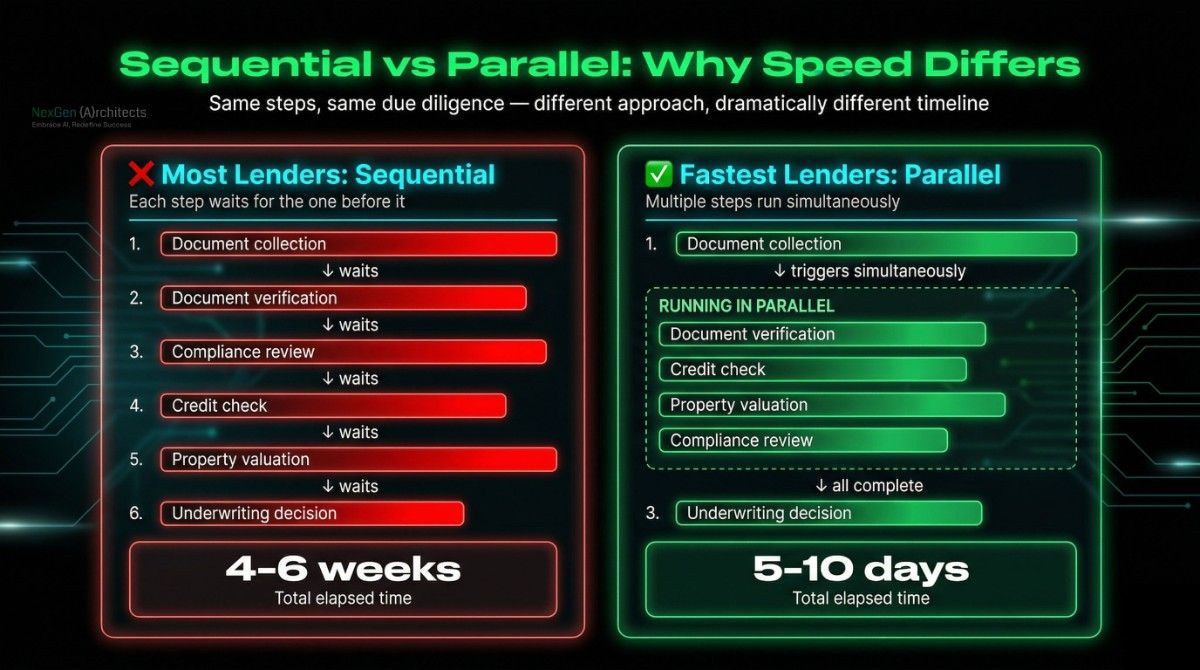

In a lot of lending operations, each step must complete before the next one begins. The application can't move to underwriting until compliance has reviewed it. Compliance can't review until documents are verified. Documents can't be verified until the borrower has uploaded them often to the wrong portal, in the wrong format, or missing a page. This sequential chain means one slow step holds everything behind it.

When different departments sales, underwriting, compliance, servicing, legal each maintain their own records, discrepancies inevitably appear:

Each discrepancy triggers a manual investigation. Someone has to stop, compare records, identify the correct version, and update everywhere it's wrong. This happens multiple times per application across most lending firms.

FCA and GDPR requirements mean every decision, every communication, and every document exchange in the lending process needs to be recorded and retrievable. In firms where compliance documentation is assembled manually screenshots, saved emails, spreadsheet logs this work is time-consuming, error-prone, and often done retrospectively rather than in real time.

In many firms, nobody has a single view of where every application stands at any given moment. The sales team sees pipeline data. Underwriting sees its own queue. Compliance has its own tracker. The operations director pieces it all together from weekly reports and email threads. This lack of real-time visibility means problems surface late, exceptions aren't caught early, and management decisions are based on information that's already days old.

The cost of slow processing goes far beyond customer frustration. It shows up across the entire business in ways that are easy to overlook individually but significant in aggregate.

In a competitive market, borrowers apply to multiple lenders. The firm that comes back first with a clear answer often wins the business. Every day an application sits in a queue is a day the borrower might accept an offer from someone else. In specialist lending bridging, commercial, second-charge speed of execution is frequently the deciding factor.

When staff spend a significant portion of their day re-entering data, chasing documents, reconciling information, and manually assembling compliance records, the cost per application rises. This is time that doesn't scale doubling application volume means doubling headcount, rather than simply processing more through the same operation.

Manually assembled audit trails are inherently risky. Missing records, inconsistent timestamps, and incomplete documentation can surface during FCA reviews or internal audits. The FCA's Q4 2025 data showed the total stock of mortgage possessions reached 7,822 the highest since 2014, and up nearly 30% year-on-year. In a market under increasing regulatory scrutiny, compliance gaps carry real consequences.

Borrowers who can't get updates on their application, who have to repeat information to multiple people, or who discover errors in their records don't stay quiet. They complain. They leave reviews. They tell their broker not to send future clients. In broker-originated lending which accounts for a large share of the UK mortgage market one bad experience can close an entire referral channel.

Firms that can't process efficiently can't scale without proportionally increasing headcount and overhead. This makes growth more expensive, margins thinner, and the business more vulnerable to market downturns.

The lending firms that consistently process faster aren't necessarily the ones with the biggest budgets or the newest platforms. They share a few operational characteristics that separate them from slower competitors.

Every team works from the same customer record

Instead of each department maintaining its own version of the borrower's information, the fastest firms have one single record that every team accesses. When the borrower updates their address, it updates everywhere. When a credit check returns, everyone who needs to see it sees it immediately. This eliminates the reconciliation problem entirely.

Instead of waiting for one step to complete before the next begins, the fastest firms run parallel workstreams:

This parallel approach can compress a multi-week timeline into days without cutting any corners on due diligence.

Instead of staff manually recording what happened after the fact, the fastest firms have systems that document every action, every approval, every communication, and every decision as it happens. When an auditor or regulator asks for the trail behind a specific lending decision, it's available instantly not assembled over several days from emails and spreadsheets.

Instead of staff logging into Equifax, Experian, or a valuation platform separately, copying the results, and pasting them into another system, the fastest firms have these results delivered directly into the application record. No manual re-entry. No transcription errors. No waiting for someone to "pull the report."

When the customer can see where their application stands what's been completed, what's pending, what's needed from them two things happen. First, they provide required information faster because they can see exactly what's missing. Second, they stop calling to ask for updates, which frees up staff time for higher-value work.

Instead of relying on weekly reports and email chains, the fastest firms give their operations directors, and compliance leads a live view of every application across the business where it stands, what's holding it up, and which exceptions need attention. Problems get caught in hours instead of days.

When processing slows down, the instinctive reaction is to hire. More underwriters. More admin coordinators. More compliance officers. More people on the phones.

But if the underlying issue is that teams can't see each other's work, that information has to be re-entered between platforms, and that processes run sequentially when they could run in parallel adding more people simply means more people navigating the same inefficient operation.

The economics are clear. UK outstanding mortgage balances reached £1,734.4 billion in Q4 2025, the highest since reporting began in 2007 (FCA). Volumes are rising. Regulatory requirements are tightening. Margins are under pressure from competition and rates. Lenders that scale by adding headcount proportionally to volume will eventually hit a ceiling where the cost of processing outweighs the return.

The firms pulling ahead are the ones that scale by making their operation faster and more accurate not just bigger.

The good news is that improving loan processing speed doesn't require replacing every platform or starting from scratch. Most firms already have capable tools they just aren't working together.

A practical starting point:

Not the idealised version in your process documents the real one. How information actually moves between teams. Where manual steps exist. Where people wait.

In most firms, a small number of manual handoffs and sequential bottlenecks account for the majority of elapsed time. Fixing those first delivers the fastest improvement.

"Can you see what the other teams see?" If underwriting can't see what compliance has already reviewed, if sales can't see where the application is in the queue, if the customer can't see what's pending those gaps are where your time is being lost.

The goal isn't to rip out existing platforms. It's to get them sharing information in real time so your teams, your borrowers, and your compliance records all work from the same truth.

Firms that approach it this way typically see meaningful improvement in processing speed, error rates, and audit readiness within weeks.

Loan approvals take too long not because lending is inherently slow, but because most lending operations are still running on workflows designed for a different era. Information sits in different places. Teams wait on each other. Compliance is assembled after the fact. And customers are left in the dark.

The firms that fix this don't just process faster. They reduce errors, lower costs, strengthen compliance, and deliver an experience that earns borrower loyalty and broker confidence. In a UK market processing over £77 billion in mortgage advances per quarter, even small improvements in speed and accuracy translate directly to revenue and margin.

The gap between the fastest lenders and the rest isn't closing. It's widening. And the difference isn't technology budgets it's whether the operation works as one or works in pieces.

.svg)